Bear of the Day: Papa John's International (PZZA)

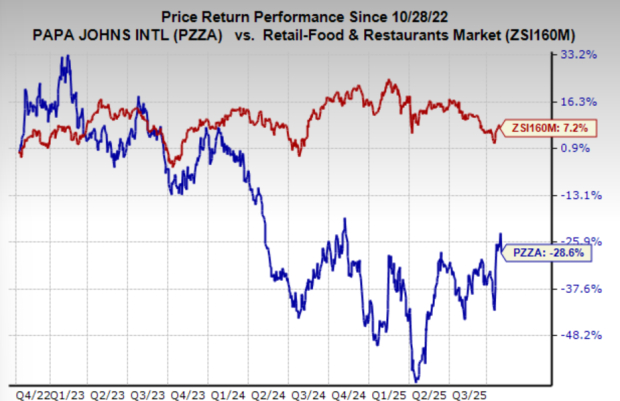

Papa John’s International (PZZA) has faced a series of headwinds in recent years, from sluggish sales growth and an elevated valuation to ongoing reputational challenges tied to its former CEO. The stock has been trending lower since early 2022, reflecting the company’s struggle to reignite momentum amid rising competition and weakening brand perception.

Adding to the pressure, analysts have steadily revised earnings estimates downward, signaling eroding confidence in near-term performance. While acquisition rumors have offered brief support, the company’s standalone fundamentals remain weak, making Papa John’s a name investors may want to avoid until its outlook improves.

Image Source: Zacks Investment Research

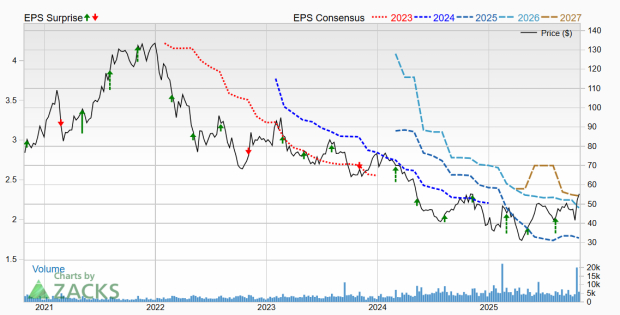

PZZA Stock Slumps on Downgrades

Earnings estimates for Papa John’s have been trending steadily lower since 2022 and were cut again over the past 30 days, giving the stock a Zacks Rank #5 (Strong Sell) rating. Analysts have reduced current year earnings estimates by 1.7% and next year’s by 4.5%, reflecting continued pressure on both sales and margins.

Revenue growth remains tepid as well, with sales expected to rise just 2.9% this year and 1.2% in 2026, suggesting limited momentum despite efforts to stabilize operations. Adding to the challenge, the Retail–Restaurants industry, of which Papa John’s is a part, currently ranks in the bottom 9% of all Zacks ranked industries, further weighing on investor sentiment and near-term performance potential.

Image Source: Zacks Investment Research

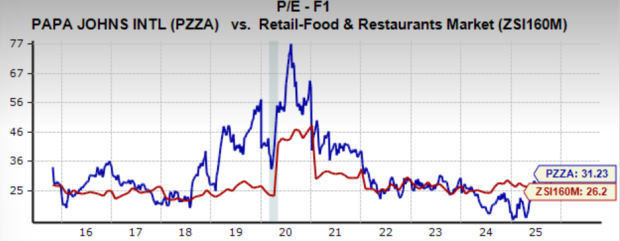

Papa Johns International Shares Trade at a Premium

Perhaps most concerning is that, despite multiple bearish catalysts, Papa John’s International continues to trade at a premium valuation. The stock’s forward earnings multiple of 31.2x sits above both the industry average and its own 10-year median of 28x.

Adding to the concern, earnings are projected to grow just 6.6% annually over the next three to five years. That modest outlook gives PZZA a PEG ratio of 4.7, an exceptionally high level that underscores how stretched the valuation appears relative to its growth potential.

Image Source: Zacks Investment Research

Should Investors Avoid PZZA Stock?

With slowing growth, falling earnings estimates, and an industry ranking near the bottom of the Zacks universe, Papa John’s International faces a difficult road ahead. The company’s challenges are compounded by an elevated valuation, leaving little margin for error even if results stabilize.

Until sales trends improve and earnings momentum returns, investors may be better served focusing on stronger names within the restaurant industry or the broader consumer discretionary sector. For now, PZZA remains a clear avoid.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power, you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Papa John's International, Inc. (PZZA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}