Bear of the Day: Whirlpool (WHR)

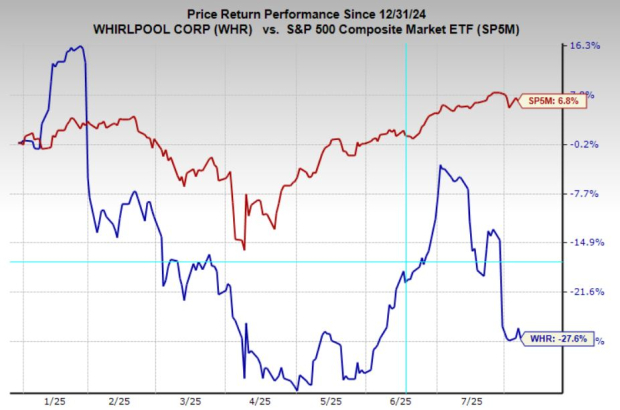

It’s been a rough year for Whirlpool (WHR). The stock is down 28% year-to-date, and the pressure shows little sign of easing. The company is facing a very challenging macro environment, with higher costs, intensifying competition from Asian imports, and soft consumer demand all weighing on results.

With considerable downside momentum, falling earnings estimates and stagnant sales, the stock is one investors should avoid for now.

Image Source: Zacks Investment Research

Whirlpool Earnings Downgrades Drag Stock Lower

The pain was underscored in the company’s latest quarterly report. Q2 revenue fell 5.4% year-over-year to $3.77 billion, missing expectations, while adjusted EPS came in at $1.34, well below consensus estimates and last year’s $2.39. Net income tumbled 70% to $65 million, and profit margins contracted sharply.

Analysts have responded by slashing their forecasts. Earnings estimates have cratered 26.6% for this year and 25.5% for next year, pushing Whirlpool to a Zacks Rank #5 (Strong Sell). Sales are projected to decline 7.2% in 2025 and another 3.6% in 2026, reflecting persistent headwinds from tariff-driven stockpiling by competitors and weaker demand.

Image Source: Zacks Investment Research

Whirlpool Shares Still Trade at a Premium

Despite these challenges, Whirlpool stock is not particularly cheap. It currently trades at 13.6x forward earnings, above the industry average of 11.2x and its own 10-year median of 9.4x. If earnings continue to fall or sentiment weakens further, that premium valuation leaves plenty of room for downside risk as the multiple compresses toward industry norms.

Image Source: Zacks Investment Research

Should Investors Avoid Whirlpool Stock?

In a more favorable backdrop, Whirlpool’s global brand and product portfolio might warrant a premium. But with falling earnings, weakening sales, and compressed margins, the near-term outlook appears grim. Add in negative free cash flow, and it’s no wonder the stock has been punished.

Until earnings estimates stabilize and management demonstrates a clear path to margin recovery, investors may be better off avoiding Whirlpool.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See "2nd Wave" AI stocks now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Whirlpool Corporation (WHR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}