How Kimberly-Clark's 'Powering Care' Strategy Is Driving Growth?

Kimberly-Clark Corporation KMB has been executing its “Powering Care” strategy for nearly two years and the fourth quarter of 2025 results suggest the initiative is gaining traction in driving growth. The company has leaned heavily on a volume-plus-mix model, which is increasingly evident in its performance.

In the fourth quarter of 2025, Kimberly-Clark delivered its eighth consecutive quarter of positive volume-plus-mix growth, signaling consistent demand across the portfolio. Organic sales growth of 2.1% was supported by a 3% increase in volume and mix, even as pricing actions weighed modestly on top-line expansion. This highlights the company’s ability to drive underlying growth despite a challenging pricing environment.

The strategy’s emphasis on strengthening value propositions across price tiers appears to be resonating with consumers. Management highlighted efforts to enhance offerings across “good, better, best” segments, ensuring competitiveness while still enabling premium innovation. This approach has supported volume growth, even as shoppers stay cautious and increasingly look for better value.

Another key pillar of “Powering Care” is productivity and cost discipline, which is enabling reinvestment into innovation and brand-building. Strong efficiency gains supported a 13.1% rise in adjusted operating profit in the fourth quarter of 2025, reflecting productivity savings and lower marketing, research and general expenses.

The company is also pivoting its portfolio toward higher-growth, higher-margin personal care categories, aligning with its long-term growth ambitions. Combined with a robust innovation pipeline, this repositioning supports sustained momentum.

Overall, Kimberly-Clark’s “Powering Care” strategy appears to be delivering measurable growth through volume gains, disciplined cost management and targeted reinvestment, even as external pressures persist.

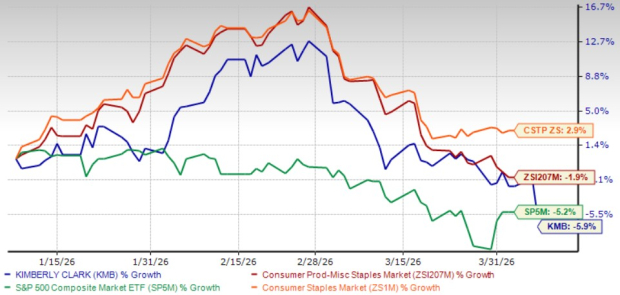

Kimberly-Clark’s Zacks Rank & Share Price Performance

Shares of this Zacks Rank #3 (Hold) company have fallen 5.9% in the past three months compared with the industry and the S&P 500 index’s decline of 1.9% and 5.2%, respectively. KMB has also underperformed the broader Consumer-Staples sector’s growth of 2.9% during the same period.

KMB Stock's Past 3 Months' Performance

Image Source: Zacks Investment Research

Is KMB a Value Play Stock?

Kimberly-Clark currently trades at a forward 12-month P/E ratio of 12.52, below the industry and the sector’s average of 17.25 and 16.29, respectively. This valuation positions the stock at a modest discount relative to both its direct peers and the broader consumer staples sector.

KMB P/E Ratio (Forward 12 Months)

Image Source: Zacks Investment Research

Stocks to Consider

Mama's Creations, Inc. MAMA manufactures and markets fresh deli-prepared foods in the United States. At present, MAMA sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Mama's Creations’ current fiscal-year sales and earnings implies growth of 39.9% and 44.4%, respectively, from the year-ago figures. Mama's Creations delivered a trailing four-quarter earnings surprise of 133.3%, on average.

US Foods Holding Corp. USFD engages in the marketing, sale and distribution of fresh, frozen and dry food and non-food products to foodservice customers in the United States. USFD currently carries a Zacks Rank #2 (Buy). US Foods Holding delivered a trailing four-quarter earnings surprise of 2.2%, on average.

The Zacks Consensus Estimate for US Foods Holding’s current fiscal-year sales and earnings implies growth of 5.4% and 20.9%, respectively, from the year-ago figures.

Tyson Foods, Inc. TSN operates as a food company worldwide. It currently has a Zacks Rank #2. TSN delivered a trailing four-quarter earnings surprise of 16.5%, on average.

The Zacks Consensus Estimate for Tyson Foods’ current fiscal-year sales indicates growth of 4.4%, from the prior-year reported levels.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Kimberly-Clark Corporation (KMB): Free Stock Analysis Report

Tyson Foods, Inc. (TSN): Free Stock Analysis Report

US Foods Holding Corp. (USFD): Free Stock Analysis Report

Mama's Creations, Inc. (MAMA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}