Integer Holdings 2026 Outlook: Drivers, Risks, Valuation

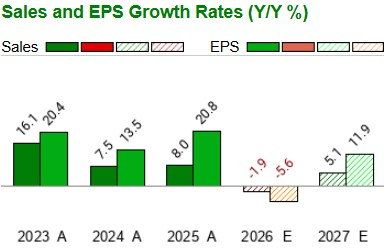

Integer Holdings ITGR is entering 2026 with a reset outlook that reflects more cautious customer signals and slower-than-expected ramps in a few newer programs. Management now expects organic sales to be flat to down 1% for 2026.

Adjusted earnings per share are expected to be in the range of $5.83-$6.40 after an April risk adjustment tied to customer forecast updates and slower ramps in new programs.

ITGR Sets the Stage With a Reset 2026 Outlook

The updated framing emphasizes execution and timing. Revenues are now expected to be in the range of $1.805-$1.835 billion, implying a 1% to 3% decline on a reported basis compared with 2025.

The profit outlook has also been lowered. Adjusted earnings per share is now expected in the range of $5.83-$6.40, implying flat to 9% year-over-year decline and reflecting the impact of customer forecast revisions and slower program ramps.

Image Source: Zacks Investment Research

Integer’s Business Mix Shows Where Growth Still Exists

Integer’s mix matters because the company’s three product lines are moving in different directions. Cardio & Vascular is the largest business, representing 59.7% of 2025 revenues. Cardiac Rhythm Management & Neuromodulation is the second pillar at 36.1%, while Other Markets is much smaller at 4.2% and shrinking as the company exits Portable Medical.

That mix showed up clearly in the first quarter. Cardio & Vascular revenue rose 1% year over year to $262 million, supported by neurovascular strength and contributions from prior acquisitions, even as certain electrophysiology programs remained soft.

Cardiac Rhythm Management & Neuromodulation revenue increased 5% to $168 million, with cardiac rhythm management growth more than offsetting weakness in neuromodulation. Other Markets declined, reflecting the ongoing Portable Medical exit and legacy manufacturing service agreements tied to divested operations.

Image Source: Zacks Investment Research

ITGR’s New Products Are the Near-Term Drag

The most immediate headwind is the slower adoption of three recently launched products. Two are in electrophysiology, and one is in neuromodulation. Management expects these programs to reduce 2026 sales growth by about 3% to 4%.

That dynamic helps explain why the outlook was tightened despite resilience in core franchises. Until adoption normalizes, the newer programs can weigh on both volume and operational rhythm, especially when customers adjust their own schedules and ordering patterns.

Integer’s OEM Forecast Swings Limit Margin Recovery

Integer’s revenue timing is highly dependent on original equipment manufacturer ordering patterns and forecast updates, particularly in fast-moving electrophysiology. Management stated that it typically has better visibility for only the next one to two quarters through purchase orders, while rolling 12-month forecasts can be revised as customer manufacturing plans change.

That limited visibility matters operationally. When ordering shifts, plant utilization can move quickly, and the company has less ability to fully control near-term utilization and margins. In the first quarter, lower fixed-cost absorption was a key factor behind margin pressure.

ITGR’s Q1 Print Shows Resilience but Not Enough

First-quarter revenues were $439.6 million, up 0.5% year over year, and exceeded the Zacks Consensus Estimate by 3%. Organic revenue increased 1.3%, indicating the core portfolio continued to hold up despite drag from new-product ramps and the Portable Medical exit.

Adjusted earnings per share were $1.20, down 8.4% year over year and a modest miss versus the consensus estimate. Profitability was the bigger issue. Gross margin contracted 260 basis points to 24.9%, and adjusted operating margin fell 230 basis points to 13.9%, due to lower absorption and higher operating expenses.

This is the crux of the near-term setup: the top line is not collapsing, but margin recovery is being delayed while utilization remains constrained and newer programs ramp more slowly than planned.

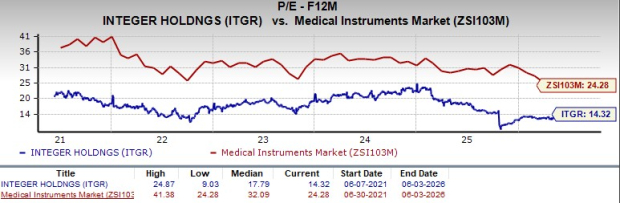

Integer’s Valuation Looks Cheaper, but the Report Is Cautious

ITGR trades at 14.3X forward 12-month earnings, below the Zacks sub-industry of 24.3X, the Zacks sector at 19.5X, and the S&P 500 at 21.9X. Over the last five years, ITGR’s forward multiple has ranged from 9X to 24.9X, with a median of 17.8X.

The discount is notable, especially as investors compare ITGR with other Medical - Instruments names such as Globus Medical GMED and Masimo Corporation MASI, which are included in the same peer set. Still, the setup remains sensitive to execution, leverage and the timing of new-product adoption. Total debt was $1.25 billion at the end of the first quarter, and the company’s debt-to-capital ratio of 0.44 remains above the industry’s 0.28.

Image Source: Zacks Investment Research

ITGR’s Bottom Line for Readers

Integer has a pipeline and partnership model that can lift growth once electrophysiology ordering stabilizes, but near-term downside risks remain the dominant factor. The path to improved utilization and margin recovery still depends on customer ordering patterns and a return to more normal ramp behavior in the three newer products.

With Zacks Rank #4 (Sell) and a $77 price target, the risk-reward profile remains pressured until electrophysiology volatility eases and adoption timing becomes more dependable.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Masimo Corporation (MASI): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Integer Holdings Corporation (ITGR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}