Is ASE Technology Becoming an Underappreciated AI Winner?

ASE Technology Holding Co., Ltd. ASX is increasingly emerging as one of the most important beneficiaries of the artificial intelligence boom, yet the company often receives far less attention than AI chip designers and foundries. As the world’s largest outsourced semiconductor assembly and testing (OSAT) provider, ASE Technology occupies a critical position in the AI supply chain, particularly in advanced packaging and testing.

The company’s first-quarter 2026 results highlighted this strength. While many semiconductor companies experienced typical seasonal weakness, ASE Technology’s ATM (assembly, testing and materials) business posted record revenues of NT$112.4 billion, up 29.7% year over year. Computing-related demand continued to expand, driven largely by AI infrastructure and advanced packaging requirements. The ATM segment now contributes about 65% of consolidated revenue and more than 90% of operating profit, underscoring its growing importance.

A major growth driver is LEAP, ASE Technology’s advanced packaging platform. Management raised its 2026 LEAP revenue outlook and now expects revenue from these services to exceed $3.5 billion. The company is also increasing capital expenditures to support stronger-than-expected demand and prepare for another major capacity ramp in 2027.

Importantly, ASE Technology’s opportunity extends beyond traditional packaging. The company is investing in full-process advanced packaging, wafer-sort capabilities, panel-level packaging and co-packaged optics or CPO, all of which are expected to play increasingly important roles in next-generation AI systems.

Financially, the benefits are already visible. First-quarter gross margin expanded to 20.1%, while net income surged 87% year over year. Management expects revenue, gross margin and operating margin to improve again in the second quarter.

While investors often focus on AI chipmakers, ASE Technology’s growing role in enabling AI hardware suggests it may be one of the semiconductor industry’s more underappreciated AI winners.

How ASE Technology Compares With Industry Peers

Two notable companies benefiting from AI-driven semiconductor demand are Amkor Technology AMKR and United Microelectronics UMC.

Amkor Technology remains one of the largest OSAT providers globally and is benefiting from rising demand for advanced packaging solutions tied to AI accelerators and high-performance computing chips. Amkor Technology continues to expand its advanced packaging footprint and strengthen relationships with leading semiconductor customers. However, ASE Technology’s combination of packaging, testing and EMS capabilities provides broader exposure to AI infrastructure spending.

United Microelectronics plays a different but complementary role in the semiconductor supply chain as one of the world's leading pure-play foundries. While United Microelectronics is not a packaging provider, it benefits from growing semiconductor content across AI, industrial and connectivity applications. United Microelectronics continues to focus on specialty technologies and mature-node manufacturing that support a broad range of end markets. As AI adoption expands, United Microelectronics stands to benefit from rising wafer demand, while ASE Technology captures value further downstream through packaging and testing services. The close relationship between foundry production and advanced packaging demand makes both companies important participants in the AI ecosystem.

Both Amkor Technology and United Microelectronics are positioned to benefit from increasing semiconductor demand. However, ASE Technology’s expanding LEAP platform, advanced packaging leadership, record ATM performance and strong visibility into 2027 growth suggest it may offer a more direct way to capitalize on the rapidly growing AI packaging opportunity.

ASX’s Price Performance, Valuation & Estimates

ASE Technology has surged a stellar 143.8% year to date (YTD) compared with the industry’s growth of 68.9%.

ASX YTD Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, ASX stock trades at a forward price-to-earnings (P/E) multiple of 32.44, below the industry’s average of 40.89.

ASX’s P/E Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

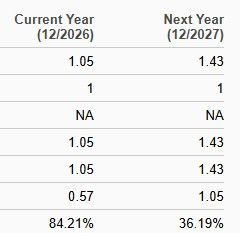

Over the past 30 days, the Zacks Consensus Estimate for ASE Technology’s 2026 earnings per share has increased to $1.05, as shown below. The estimated figure calls for 84.2% growth from 2025.

EPS Trend of ASX Stock

Image Source: Zacks Investment Research

ASX’s Zacks Rank

ASE Technology currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

United Microelectronics Corporation (UMC): Free Stock Analysis Report

Amkor Technology, Inc. (AMKR): Free Stock Analysis Report

ASE Technology Holding Co., Ltd. (ASX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}