Is NVST Attractive at 15.1x Forward Earnings?

Envista Corporation NVST has started to rebuild investor confidence, but the valuation question is still front and center. The stock trades at 15.1x forward 12-month earnings, a modest premium to its Zacks sub-industry at 14.9x, and a discount to the Zacks sector at 19.6x and the S&P 500 at 22.2x.

Image Source: Zacks Investment Research

With shares at $22.94 and a $24 price target tied to a 16.2x forward 12-month earnings multiple, the setup is about whether recent execution can hold long enough to justify a slightly higher multiple.

NVST Valuation Setup Using the Report’s Multiples

The market is assigning Envista 15.1x forward 12-month earnings. That level sits close to the sub-industry’s 14.9x, implying investors are not yet paying up for a decisive re-rating. At the same time, the discount to the sector (19.6x) and the S&P 500 (22.2x) suggests expectations remain restrained.

The $24 price target is anchored to a 16.2x forward 12-month earnings multiple, which is only modestly above today’s trading level. Put differently, the upside case is not dependent on a big multiple expansion. It depends on Envista sustaining the operating improvements now showing up in results.

Envista Price Performance Context and What It Can Mislead

Envista shares are up 5.7% year to date and up 22.3% over the past year. That performance looks more constructive when set against a weak peer backdrop: the Zacks sub-industry is down 25.2% year to date and down 30.9% over the past year, while the Zacks Medical sector is down 6.6% year to date and up 2.7% over the past year.

Benchmark dispersion matters because multiples are forward-looking reflections of market expectations. A sub-industry drawdown can compress peer multiples even if fundamentals differ, while a more resilient sector line can keep sector-level valuations elevated. Against that backdrop, Envista’s near-sub-industry multiple reads less like “cheapness” and more like a market that wants proof the recent momentum is repeatable.

NVST Earnings Power: What Q1 2026 Revealed

The first quarter of 2026 showed meaningful profit acceleration alongside solid top-line growth. Revenue was $705.5 million, up 14.4% year over year. Adjusted diluted earnings per share were $0.36, up 50% year over year, while GAAP diluted earnings per share were $0.23.

The quality of the improvement matters. Adjusted gross margin expanded 100 basis points to 55.8%, supported by volume, price, productivity and favorable foreign exchange. Operating expenses also grew more slowly than revenue, with selling, general and administrative expenses up 9.5% to $297.6 million, even as research and development spending rose 18.6% to $30.0 million.

NVST 2026 Outlook: What Must Go Right

Management maintained its full-year 2026 outlook for core sales growth of 2% to 4%. The Zacks Consensus Estimate calls for $2.86 billion of revenue, implying 5.1% growth from the year-ago reported figure. That gap sets up a clear “meet the bar” framework: the market will watch whether reported results can track closer to consensus while still fitting inside the company’s core-sales lens.

Earnings expectations are similarly defined. Adjusted diluted earnings per share are expected to be between $1.35 and $1.45, while the Zacks Consensus Estimate is $1.43. With the stock priced off forward earnings, execution against that range is a key driver of whether the multiple holds.

Envista Rating Lens for Near-Term Decision Makers

For investors using a shorter time horizon, the Zacks Rank provides the primary signal. Envista currently carries a Zacks Rank #3 (Hold). The Style Scores show what the model is rewarding: VGM is B, with Value at B, Growth at C and Momentum at B.

That mix fits the current setup. The Value and Momentum profile aligns with a stock that has improved and is not priced like a sector leader, while the weaker Growth score reflects the need for continued follow-through in demand, share gains and operating leverage.

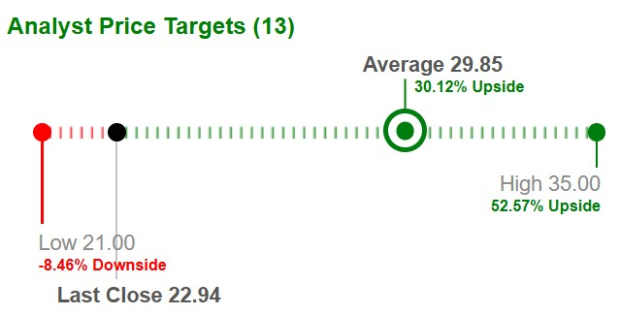

Based on short-term price targets offered by 13 analysts, the average price target of $29.85 represents an increase of 30.12% from the last closing price.

Image Source: Zacks Investment Research

NVST Checklist: What Would Change the Multiple

A practical catalyst list starts with tariffs. Tariff costs increased $11 million year over year in the first quarter, but were offset by supply chain, general and administrative, and pricing initiatives. Sustained offsetting through pricing and productivity is central to protecting margins as similar quarterly levels are anticipated through 2026.

Next is adoption. Recent launches include the Nobel S Series in implants, the Spark clear aligner launch in Japan, and DEXIS software enhancements adding artificial intelligence-driven workflow and diagnostics tools. Progress in China implants is also key, with uncertainty tied to expected volume-based procurement timing that management expects to begin between the second and third quarters.

What could break the thesis is straightforward: weaker-than-expected traction for new products and software, higher tariff drag that outpaces mitigation, or macro softness that slows dental utilization and purchasing cycles.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Envista Holdings Corporation (NVST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}