Palantir Stock's Valuation: Overstretched or Rightfully Earned?

Palantir Technologies PLTR has emerged as one of the most talked-about names in the S&P 500, and not just for what it does, but for what investors are willing to pay for it. With a market capitalization of $422.5 billion, it now surpasses giants like Coca-Cola and Bank of America. Yet, when viewed through a valuation lens, Palantir stands alone in its league.

Its trailing 12-month price-to-earnings ratio exceeds 546X, and its forward 12-month multiple hovers above 180X. Even more striking is its enterprise value relative to forward 12-month revenues of nearly 70X, a level rarely seen, even during the most exuberant periods in market history.

Such elevated valuations raise the bar for future performance. For a company trading at these levels, expectations around revenue acceleration, margin expansion, and long-term scalability must not only be met but also exceeded. Even minor disappointments can trigger sharp corrections as multiples revert toward historical norms. Companies in the past that reached these kinds of revenue multiples, often 30X or higher, eventually faced tough questions about sustainability. Optimism alone is rarely sufficient when fundamentals lag.

That said, Palantir’s expanding government and commercial contracts, its robust and evolving AI platforms and consistent execution lend credibility to its premium valuation. While risks remain, we view Palantir as one of the most compelling long-term AI plays available today.

PLTR’s Price Performance, Estimates

The stock has surged a whopping 130.5% over the past year, significantly outperforming the industry’s 4% rally.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

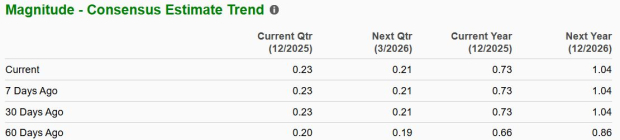

The Zacks Consensus Estimate for PLTR’s 2025 earnings has increased 10.6% over the past 60 days.

Image Source: Zacks Investment Research

PLTR stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Stable Defense Alternatives to Palantir

As PLTR’s valuation moves higher, Lockheed Martin LMT and RTX Corporation RTX offer more grounded defense exposure. Lockheed Martin, with its massive defense contracts, provides steady cash flow and less volatility than PLTR. Its trailing 12-month price-to-earnings ratio is just above 16X, and its forward 12-month multiple is just below 16X. Lockheed Martin continues to benefit from global rearmament while trading at modest earnings multiples.

Similarly, RTX shines through missile systems. RTX’s defense backlog, like LMT's, underscores its stability. Its trailing 12-month price-to-earnings ratio is above 28X and its forward 12-month multiple is above 26X.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lockheed Martin Corporation (LMT): Free Stock Analysis Report

RTX Corporation (RTX): Free Stock Analysis Report

Palantir Technologies Inc. (PLTR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Source Zacks-com

{kind=link}

{kind=link}

{kind=link}